We’re Entering Untested Entertainment Territory

“Ventress wants to face it. You want to fight it. But I don’t think I want either of those things.” – Josie Radek, “Annihilation,” Paramount, 2018

Depending on which segment of the film/show industry and your organization, things are good, pretty good or not so good but looking up according to the folks on Wall Street.

Theaters expect to bring in $42+B in revenue this year even though they still complain that their theatrical windows are too short.

Oh sure, the actual number of tickets sold were still off, but they still expect to gross $44B in 2026. No, the growth isn’t magic or cooking the books. All you have to do is charge more for the tickets (especially for the big hitter projects), bump up the cost of concessions a little and sell more greasy popcorn and sugared water drinks.

Patient Care – Film production is suffering in the US, especially in Hollywood where shoot days are off dramatically. Greenlighted projects have smaller crews and lower budgets this year.

Even though movie production is down – again – in Hollywood from its peak TV levels by 40 percent; the home of the famous production companies, the US, will still manage to deliver 1,523 movies this year plus a wide assortment of TV shows.

India, the world’s second-oldest film production country, delivered more films/shows – a lot more – followed by the UK, China (most available only locally and SEA -Southeast Asia), France, Japan, Germany, South Korea, Canada and Australia.

The slow decline of ticket sales never bothered studios before because they could count on booster shots from broadcast and cable networks.

You know, 500 channels to flip through but still nothing to watch.

But at least you didn’t have to jump into and out of the different channels. You only had to scroll through the EPG (electronic program guide) to find the movie you heard was good, show you wanted to catch up on or the neat out-of-the-way project you were interested in.

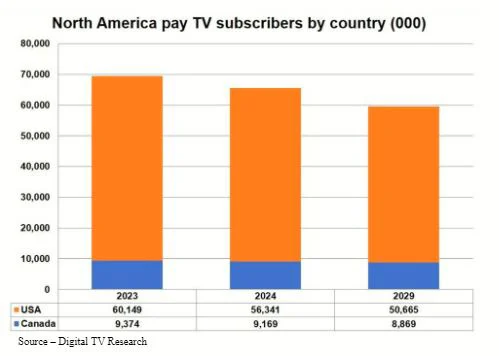

Issues Hit Home – The cost of fixed TV bundles with a major amount of unviewed channels, the lack of new/interesting content and fixed programming have taken a toll on pay TV subscriptions as people move to more economic, flexible entertainment options. The bundles won’t disappear but will be less important to younger generations.

But the bundle was taking too much out of the family budget and people wanted a better, less expensive option for their home entertainment.

On Demand – Consumers in developed countries quickly began to prefer streaming services that delivered entertainment when you wanted and where you wanted it. People in developing countries are increasingly moving from their pay TV as well.

VOD (video on demand) “suddenly” became the home entertainment resource of choice–especially when you could watch what you wanted, when you wanted, on the screen you wanted, and the cost was less than 10 bucks a month (in the Americas).

A helluva deal.

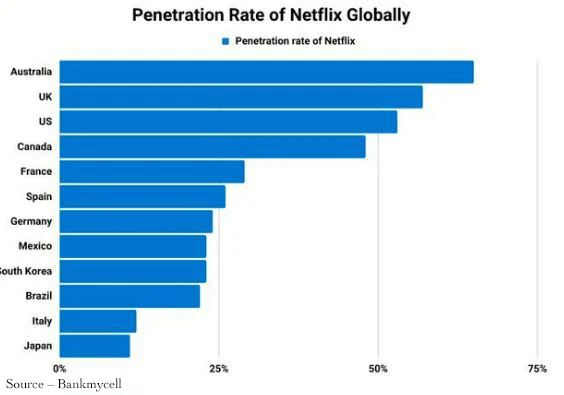

No wonder Netflix grew from the tech company all of Hollywood looked down on – and were more than willing to make and sell content to – until the company became the clear and undisputed leader of streaming video that recently reported they had nearly 264.5M subscribers in 190 countries around the world.

Somehow, the stalwart Silicon Valley company had figured out how once film/show production shifted to digital that VHS, DVD, Blu-Ray were just stepping stones in the shifting entertainment landscape to personalizing content and entertainment delivery.

Of course, they also had a secret technical advantage.

Yep, they had data on the shows/movies people watched, how long they watched it and the screen they watched it on in every region of the globe.

Leader – Using regional and global viewer content interest and data, Netflix continues its streaming leadership by mixing movies, shows, live events and more to provide subscribers with local and international entertainment.

They continue to keep their foot on the gas to maintain their leadership in the streaming arena, constantly investing in new and acquired projects (shows/movies) until they slowed down.

It wasn’t because they needed to show Wall Street profits because they have been and are.

They released 92 original seasons this year, down slightly from the prior year, along with a slew of acquired titles including a number of international titles that grabbed viewer interest/attention regardless of their home country.

In addition, they broadened their offerings with live events like boxing, WWE, wrestling and NFL football with more sports and live events sure to follow.

They probably would have liked to have some of the Euro 2024 and Copa America futbol action which was huge everywhere but North America where the sport is consistently misspelled.

Back for More – People may run through the shows/movies they’ve just got to see but live sporting events keep sucking them back into the various services they subscribe to. Some events are just too important to miss.

But there’s always next year and other sport contests that suck people in who have to watch.

In addition, they surprised Wall Street (and the competition) by clamping down on password sharing, gaining subscribers rather than losing viewers. There’s more work to be done in weaning folks off the sharing habit but they’re doing it professionally and the content consuming public is coming around.

Actually, they are the only true streaming entertainment service but then:

- We know YouTube is a streamer (and a huge one), but we still find it hard to view them as a real content development, creation, production, delivery company but rather an ad company that makes money from the stuff the creator generation puts up

- Prime is a close number 2 to Netflix and does greenlight/acquire a lot of content, but profits are less clear because of their ecommerce/cloud services

- Apple TV+ is a class act but profit (or loss) is hidden inside a myriad of great products and services so…

Of course, the minute the Hollywood studio/network crowd (Disney, Warner Bros, Paramount, Peacock and their related operations) saw how quickly families in North America and around the globe were cutting back/off Peak TV, they moved to develop their own day/time/screen options.

Mud Fight – Studios and networks have gone all in to capture a major (and profitable) share of the streaming video market but it’s still a work in progress to grow subscription rates while balancing legacy requirements.

But it hasn’t proven to be as easy as they and the 200 other streaming services around the globe envisioned.

Ninety plus percent of the households in North America have at least one subscription streaming service; and while cost is an important factor, the average number of services families subscribe to is 4.3.

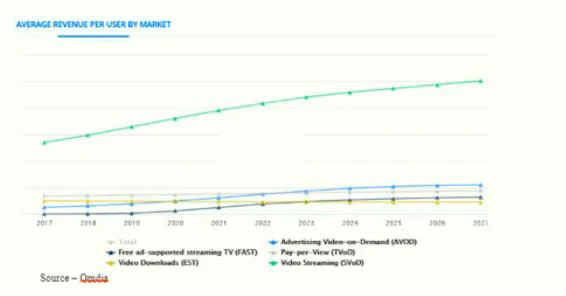

According to PwC, global subscriptions for ORR services will rise from 1.6B last year to 2.1B by 2028. Global revenue per subscriber is expected to grow from $65.21 to $67.66 by 2028.

To increase their subscription numbers while maintaining/increasing profits, all of the streaming services – except for Apple TV+ (for the time being) – streamlined their subscription categories and added an ad-supported option.

Yeah, we know Netflix said never ads, ever, but that was yesterday, and this is today.

The minute they did, we immediately switched four of our five services to AVOD because well, we like ads and three-four minutes (max) of ads an hour vs. 18-20 minutes feels like no ads and honestly, we like a little break in the intensity of the movies/shows we watch.

Options But – Consumers will tell you that the cost of their streaming service is the most important consideration but still, people seem to prefer uninterrupted content viewing, at least for their main streaming service and a lower cost for “fill in” entertainment.

As for “normal” people; well, they surprised us.

It turns out that for the time being, most people prefer not to have their movie/show interrupted; but more importantly, viewers know precisely what they want.

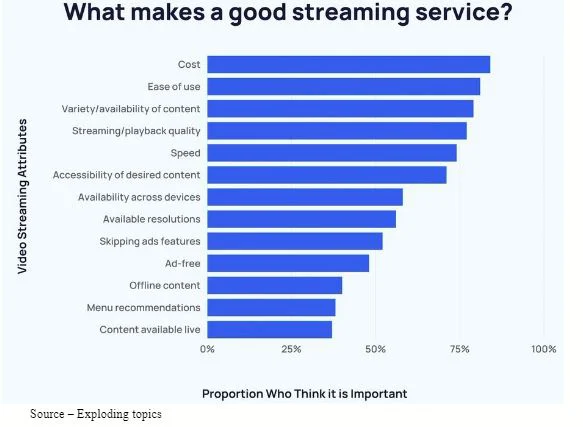

Selection Process – The selection of streaming video services people will subscribe to relies on a number of factors including content library, quality of viewing, ease of finding interesting shows/movies and yes, cost.

Sure, cost is important but there but there are features that add value to the services they subscribe to including availability of “new” theatrical releases, all of a shows seasons, original movies/shows, as well as features which technically-based companies fully embraced at the outset including streaming quality/speed and high-quality resolution regardless of where they are located (hence delivery servers in key locations around the globe).

In addition, a robust recommendation menu and engine that understands the viewer’s entertainment likes/dislikes so it can intelligently recommend movie/show options when you simply tune in to watch “something” and BAM! you actually get something you didn’t know you really wanted to watch.

Yes, we know it’s AI-based (one of the few applications we trust) that does one thing, does it well and we don’t have to chat with it. But while subscription-only may continue to be the largest portion of the home/personal content viewing, we still feel that ad-supported will become more important and valuable to streaming services.

Streaming Revenue – One size, one option doesn’t meet everyone’s entertainment needs. People will choose services that meet their interests and budgets. And there’s plenty of room for global growth by large and small services

PwC, Ampere Analytics and a number of other industry followers project that ad revenues will hit $1T by 2026 and will account for 55 percent of the industry’s growth over the next five years. By 2028 it will account for more than 77 percent of the total ad spend.

It will grow as the industry improves its ability to monetize data and develop a closer, more refined/accurate relationship between product discovery and actual purchases.

But the burning question for us is how well the Hollywood studio/network streamers respond to take advantage of tomorrow.

People have no problem dropping Disney +, Max, Peacock or Paramount + after streaming all of the services content that interests them for another service and then returning later when new content is available–especially when the SVOD fees are already at the upper end of the budged scale.

Disney has made its service more valuable to the consumer by developing its own bundle – Disney +, ESPN and Hulu.

Legacy Growth – Hollywood studios/networks have to balance theatrical, pay TV channel and the expansion into the new streaming market profitably and it’s difficult to keep current revenue streams afloat while investing in tomorrow’s growth opportunities.

WBD’s David Zaslav is rethinking his comment at the beginning of their streaming venture when he said people would be willing to pay “a little more” for Max because they have such valuable content.

With its stock at an all-time low – down 70 percent from the merger – and the industry in what one executive at this year’s Sun Valley Billionaire summer camp called a full-scale depression, Zucker is faced with some critical decisions.

His moves will include something he’s very good at, downsizing staffs across the board – Warner Bros, Turner, Discovery, HGTV, CNN and other divisions.

The mix of legacy cable networks and streaming doesn’t exactly fit in today’s digital age which could mean asset sales, strategic partners, total restructuring while trying to understand/invest in a global streaming which requires consistent investment in new projects that resonate with subscribers.

Paramount Global is grappling with the similar problem of linear TV decline, the need to pivot to streaming plus at least a year of wading through the complex merger with David Ellison’s SkyDance Media.

What they’ve got so far is a new logo.

One of the first things Ellison and RedBird Capital’s CEO Jeff Shell, former CEO of NBCUniversal, will have to do is figure out what to do with the triad presidents Shari Redstone named prior to the acquisition as well as develop a plan of action to reinvigorate the creative side of the company.

Ellison will also have to infuse more technology into the operation, which is something he is intimately familiar with as the son of Oracle’s founder, Larry Ellison.

Peacock, the streaming service owned by NBCUniversal Media which is in turn owned by Comcast, is the smallest of the “major” streaming services with 34M plus subscribers.

A relatively stable organization, it has the advantage of Comcast’s global internet and relationships to make measured moves to profitability. In other words, we can expect the Hollywood studio/network competitors to continue to flail as they struggle to complete with and replicate the tech leader’s streaming growth and business models.

When we look at the complete entertainment arena – movie houses, Peak TV and streaming, we’re reminded what Lena said in Annihilation, “It’s not destroying. It’s making something new.”

And don’t let “industry experts” kid you.

Just remember what Dr. Ventress added, “We have many theories, few facts.”

But it’s going to be great for the content development, creation, production, delivery folks and the viewing public!